A 6 to 12-minute read – depending on your speed. This is the last of four ‘About Money’ articles on how to choose the right boxes for your money.

Here, we’ll complete our eight-point FILTRATE checklist – and so, equip you to assess any financial product (or strategy) that anyone could ever put to you.

What we’ve covered and what’s coming up

In this series, we’ve seen:

- Why professionals use checklists in all complex environments.

- Exactly how complex the money box landscape is.

- Where this task (of selecting money boxes) fits in the broader process of designing your financial life plan.

- Why it’s your ideas (for what you want to have, become or do in the future) that determine the money boxes you need.

- The eight-point FILTRATE checklist – in outline at least.

- Why there’s no such thing as a perfect money box for everyone.

- That your unique circumstances and ambitions make your (money-box feature) priorities unique to you, too.

- This means you can’t take shortcuts, and you need a checklist to consider the pros and cons of your options.

- That a solid checklist could save you, your friends and family (and thousands of others) from losing life savings to scammers.

So, if you’ve not yet done so, read those first three ‘About Money’ articles before this one.

Here, we’ll complete our detailed look at the FILTRATE checklist with examples of how each check could help you choose the right boxes for your money.

So, let’s get back to this now, with the next check on our list, which begins with the letter ‘R’.

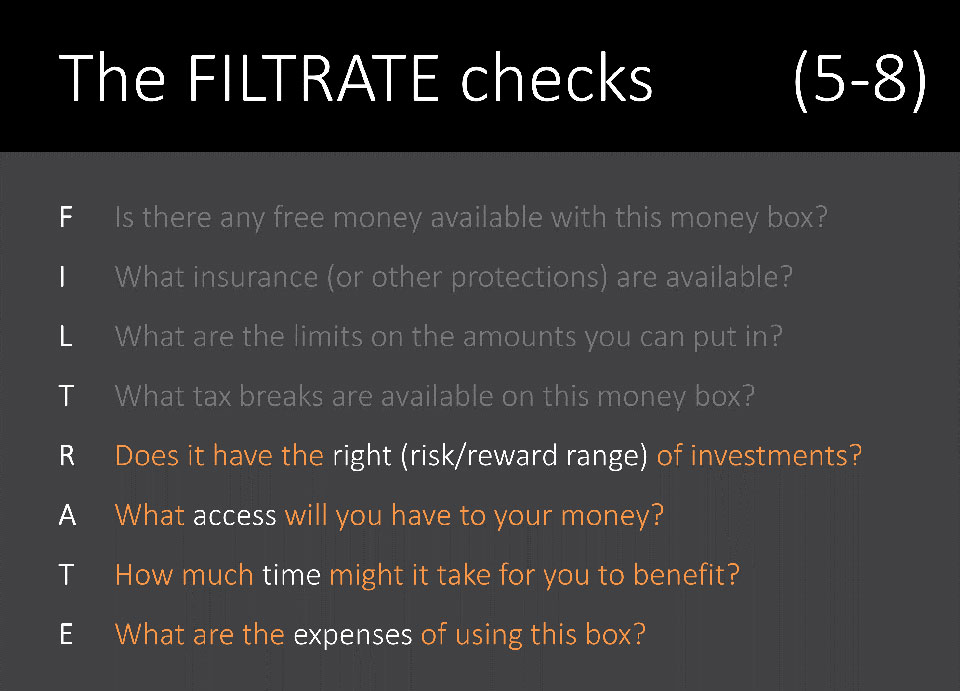

Check ‘R’: Does this money box have the right (risk/reward) range of investments?

Check ‘R’ will remind you to look at whether the money box (or strategy) you’re considering offers the range of investments (and investment funds) you need to have a good chance of achieving your goals.

For example, let’s say you have a ten to thirty-year plan to build a retirement fund.

In this case, you’ll want a money box that allows you to invest in stock market-type funds for their high long-term growth potential.

Alternatively, if you’re saving to build a deposit to buy a first home, a simple and secure cash ISA might be what you need for that goal. (And, if you’re eligible for it, you may wish to consider a Lifetime cash ISA, where your funds are boosted by a 25% free bonus from the government)

The question of how much to invest into stockmarket-type funds depends, in part, on the number of years you have to reach your financial goal. And we answered that question in detail in another series of ‘About Money’ articles here.

Investor Protection issues

We touched on investor protection under the ‘Insurance’ check and may expand on this in the future. For now, note the need to:

- Consider the financial stability of the bank, fund manager, or other organisation that will hold your money.

- Avoid exceeding the deposit protection limits on the money you hold in one banking group.

- Be extremely sceptical of any projected investment returns that look too good to be true!

Remember that Bernie Madoff promised high returns and very low risk in his ‘scheme’.

However, as anyone with a basic knowledge of finance knows, you cannot have both of those things. So, foul play should have been suspected by more people – much earlier than it was.

Investment funds authorised by the UK’s financial regulator (The Financial Conduct Authority – FCA) offer protection (up to certain limits) under the Financial Services Compensation Scheme if the investment company becomes unable to meet its legal obligations to you.

Note, however, that investment funds are not responsible for falls in the price of legitimately held investments. Nor are they responsible for market-wide falls in the prices of shares and other securities.

So, take care to invest in well-diversified funds with risk/reward ratings that are suitable for your personal financial goals.

And think seriously about the risks of not taking regulated financial advice. You cannot claim compensation if you lose money from bad advice you’ve given yourself.

A word about gearing

Are you considering an investment in property, with most of the funds coming from a mortgage? If so, you need to understand the concept of ‘gearing’.

Gearing can be a friend or a ghastly enemy to your money, depending on how asset prices move while you’re invested.

The details are complicated, but in short, a geared investment can deliver profits (or losses) as a multiple of the money you invest upfront.

For example, if you put down a 10% deposit to purchase a property, your returns are geared by a factor of 10.

For the maths-minded – the gearing factor is the reciprocal of the deposit percentage.

So, if you put one-fifth down as a deposit on a property purchase, your gearing factor is five. A deposit of one-tenth (10%) gives you a gearing factor of ten – and so on.

Here’s what this means, in practice (and before transaction costs – which may be significant): if your deposit is 10% – so your gearing factor is 10:

A 20% rise in your property price will deliver a 200% (10 times 20%) return on your deposit.

- A 20% fall in your property price will result in a 200% loss on your 10% stake. So, your deposit is wiped out, and you now owe 10% more than your property is worth. And this ghastly situation is known as negative equity.

Geared investments of all kinds (mortgaged investment property is only one example) should, therefore, be treated with caution.

Check ‘A’: What access will you have to your money?

Check ‘A’ is about the access you’ll have to your money while it’s held in the money box and/or investments you’re considering. And there are two questions about accessibility to ask:

The first is about the features of your chosen money box; the second is about the assets you place in it.

Let’s start with the money box restrictions and look at pensions as an example.

A personal or workplace pension won’t normally give you access to your money until you’re in your mid to late 50s. And this fact concerns a lot of people in their twenties or thirties.

However, this age-related access restriction may feel like far less of a problem if you’ve:

- Built up enough funds in accessible savings accounts – to cover emergencies and your other near-term plans.

- You’ve adequately insured your health and life against disasters.

This way, you (or your loved ones) will have no short-term need for the money you’re saving into pensions for the long term.

In the unlikely event that you suffer a long period of serious ill health, you may be able to access your pension benefits earlier in any event. However, the wisdom of doing so will depend on various factors – including the type and terms of your workplace pension if you have one.

You’ll also want to weigh up the potentially significant advantages of:

- Tax relief – which effectively reduces the personal cost of saving into a pension.

- Any free money paid into a workplace pension from your employer.

In a matched contribution pension scheme, you might get £2,000 paid into your pension pot at a personal (net of tax) cost of £800 – or less if you’re a higher-rate taxpayer.

That’s a seriously good investment – even if you must wait for the benefits.

Also bear in mind that many people see the age restriction on access to pension funds as a positive!

After all, having no access to these savings in the near term means you’ll have substantially more savings available when you need them to slow down or stop work in your later years.

Remember the golden rule

We should always keep in mind that there are no golden rules in financial planning.

A pension money box is certainly attractive in many situations, but that doesn’t mean it’ll be the first choice of savings vehicle for everyone.

Let’s take our earlier example of someone in their 20s who is renting a flat, has about £200 per month to save and is self-employed – which means they’ll not receive any employer contribution to their pension.

A Lifetime ISA (LISA) money box might serve them better than a personal pension because:

- The 25% (free-money) bonus on the LISA matches the upfront tax relief on a pension.

- They can access their money to purchase a first home in the very short term.

The second question on accessibility concerns how easy it might be to sell an investment when you need the money—a feature the experts call liquidity.

For example, you may find it difficult to quickly sell a residential or commercial property (for the price you want) during a severe downturn in the economy.

Also, be aware that some investment funds (which hold property or other illiquid assets) may reserve the right to delay your request to cash in (or switch out of) shares in those funds – at times when it’s difficult for the fund manager to sell the underlying assets.

Conversely, investment funds holding well-diversified portfolios of shares in publicly quoted companies do not tend to have such liquidity issues.

In short, you need to check and understand the possible access restrictions both on the money box you choose – and on the investments you plan to hold in those boxes.

Check ‘T’: How much time could it take for you to benefit?

In a world where most things can be delivered to our door in a matter of days (or minutes for fast food), it’s worth considering how long we may need to wait to benefit from the investments in our money boxes.

You probably know that, in normal times, you’ll be offered a higher rate of interest (compared to immediate access savings) by tying your money up in savings bonds for one to five years.

To enjoy potentially higher returns (from stock market-based funds), most advisers suggest a minimum term of five to seven years – because the price of these funds tends to go up and down a lot in the short term.

Then, there are other investment products which offer guaranteed minimum returns which typically only apply if you hold the investment for a certain period of time – to maturity.

And remember, on pension annuities, the income payments are guaranteed to continue for the whole of your life but may stop (immediately) if you die unexpectedly, a short time after your income begins. So, if you purchase an annuity with some of your pension pot at retirement, you may want to choose a guaranteed time period – to ensure the annuity pays out a residual sum to your heirs – in the event of an untimely death.

Finally, regarding ‘time’ questions, you should consider whether this is the right time to make the financial transaction you’re considering.

For example, you may wish to prioritize tasks to fill any serious gaps in your financial life plan, particularly if you don’t yet have the levels of life or ill health insurance that you (or your loved ones) might need.

While other tasks (like developing a sustainable retirement income plan) could benefit from you taking more time in the planning.

And in both cases, most people benefit from taking good quality advice.

Check ‘E’: What are your expenses for planning and managing your money?

The last of our eight (FILTRATE) checks relate to the expenses you pay for your money boxes, the investment funds inside them, and any financial planning advice.

In short, you want to check that those expenses are clear and reasonable for the quality and level of services you receive.

The total effect of charges on your money should be easy to find in the pre-sales notes you’ll receive on any UK-regulated investment or pension product you buy.

However, it can be more difficult with other investments, where you’ll need to add up the effect of various charges for buying and selling the investment and for its ongoing administration and management.

With direct investments into property, the total of all these charges can be significant, and you’ll need reasonable number-crunching skills to add them all up.

So, if that’s not your favourite pastime, get professional help with that.

Making good decisions about the money boxes and investment funds you hold (and the advice you take) could save you from a personal financial disaster and save you many thousands of pounds (in excessive expenses and/or taxes) over time.

Just bear these points in mind:

- Expenses (for administering a money box, for managing the investment funds within it and for financial advice) can vary – quite a lot.

- Cheap products are not necessarily good value – and the most expensive products are not necessarily the best.

- Leading product providers are seldom the cheapest or most expensive.

- If you need advice, choose someone with sound knowledge and high competence in the areas where you need help – and be prepared to pay a fair price for that.

How will you now use these ‘About Money’ articles?

You might want to share this series (with this link to the first ‘About Money’ article) with friends and family – to help them avoid scammers and choose the right boxes for their money, too.

Remember, this money-box checklist will work for people of all ages.

And, if you decide to take financial advice (for the first time or to review some plans made previously), you could use this checklist to prepare some questions for that meeting.

Either way, we hope you found some valuable pointers in this series, and we’d love to hear your comments below or by e-mail.

Thanks for dropping in.