This 10 to 20-minute read is the second of two ‘About Money’ articles for anyone who struggles to talk about (and deal with) personal money matters.

And that’s most of us from time to time!

Here, we’ll explore another five (of ten) reasons we might find it hard to talk about money, whether with close friends, family or a financial professional.

You can read the first five reasons we don’t talk about money here.

Could there be more than ten reasons?

Yes, absolutely. There may be many more reasons why we don’t have productive conversations about money, and if you struggle with this, we’d love to hear from you.

We’ll happily (and anonymously) add more blocks to our lists when we revise them.

Of course, excellent financial education enables us to make better money decisions.

We’ve known for 50 years (from the work of psychologist Albert Bandura) that we’re more likely to engage with tricky tasks when we feel more capable of them.

So, we’ll share more ‘About Money’ articles in future to help you make sound money decisions.

Now, let’s continue with our list, and explore reasons 6 to 10 for why we don’t talk about money.

Reason 6: We have an unhelpful attitude to money

Most of us form attitudes to crucial questions based on flawed or incomplete information at various points in our lives.

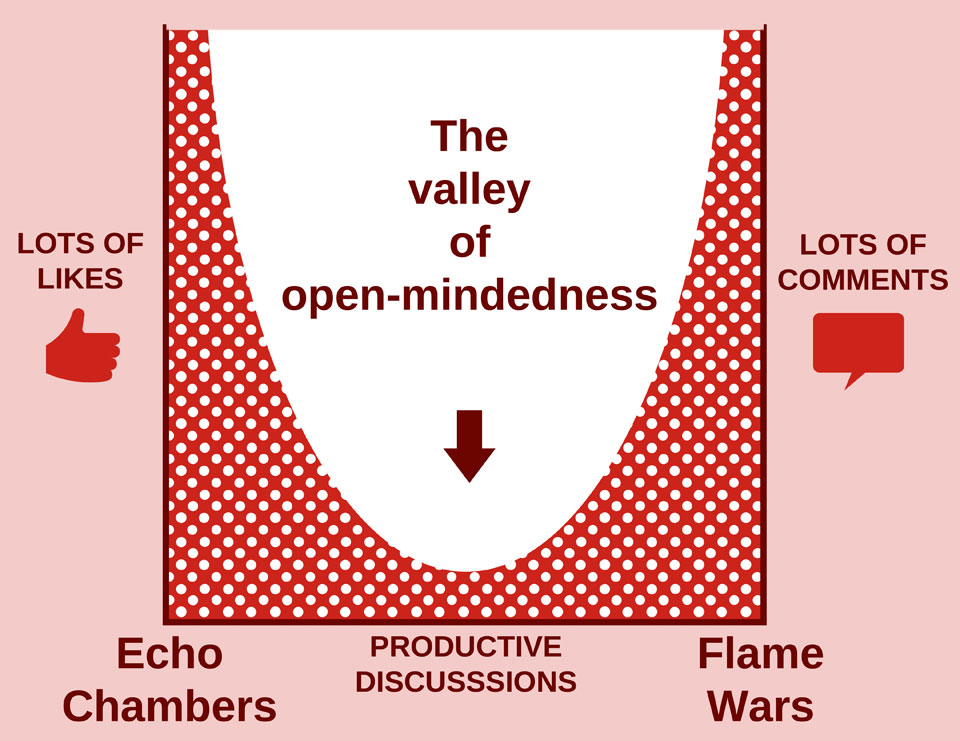

It’s easy to form simple binary (good or bad) views on most topics, but these attitudes undermine any sensible conversation.

And, we can see this play out on Social Media every day.

So, it’s worth knowing something about ‘attitudes’, which Psychologists describe as having three (ABC) components:

A reminds us of the Affective component: how our feelings affect our attitude, and vice versa.

B is for the Behavioural component: our behaviour affects our attitude, and vice versa.

C is for the Cognitive component: what we believe and know (about the ‘thing’ under discussion) affects our attitude – and vice versa!

The letters ABC are undoubtedly easy to remember, but we doubt many people remember what those psychology-technical terms stand for.

Also, thinking about the ABC elements in that order may not be the best way to change our attitudes where we need to.

It seldom helps to start by focusing on how we feel about an issue – as that can lead us to justify our thoughts.

Often, it’s best to start with ‘C’ (the Cognitive component) and fact-check our beliefs to determine if we’re falling into this thinking trap!

It seems that Mark Twain and many others observed the Dunning-Kruger effect – mentioned in the first of this two-part series more than one hundred years before the researchers found it!

We can all think of examples where changing a flawed belief could improve someone’s life or the world, right?

So, let’s keep the language simple – an ‘attitude’ is just a package of beliefs and thoughts, and the emotions and behaviours that typically result.

And the good news is – we can change our attitudes.

We acquire our attitudes from what we learn – at home, at work, and in our local and online communities.

So, we can unlearn these attitudes, too – if we need to.

Each of us has our own unique mix of (positive, neutral or negative) attitudes towards most things.

For example, how do you think, feel and act towards (and talk about) the following:

• Your role and hours at work.

• Your boss or another colleague at work?

• The behaviour of loved ones at home!

• Government policy – on health, education, transport or policing, for example.

• The behaviour of those in different political or religious groups.

The list is endless, and our attitudes to money questions vary enormously also. For example, you might believe (or not believe) that:

• It’s essential to save for a rainy day.

• It’s important to insure your life and health against an unexpected disaster.

• There’s value in taking professional advice.

If you’re fascinated by how we form our attitudes – sign up for our Newsletter to learn more about this.

We plan to share a proven life-story mapping exercise to help you discover how your unique life experiences have affected your attitudes to money.

And, of course, we’ll touch on how you might change any attitudes you need to.

Just be aware that it can be extremely challenging to change some of our attitudes, particularly those we learned in our younger years. It was then, for better or worse, that we first formed many of our attitudes to the big questions: about work, money, health and relationships.

So, please be patient and kind to yourself if you’re striving to change some of your attitudes. And remember, with regard to our money-life experiences:

• We seldom learn much from getting lucky with money.

• We don’t always learn good lessons when we’re unlucky, either!

So, it’s worth learning the essentials about money in a safe environment like this – rather than taking big risks on things you don’t understand.

Reason 7: We’re embarrassed to talk about money

Sharing our financial details with others can feel like having guests come to our home for dinner. We don’t want them to see the mess that our children (or we!) usually make around the house, so we rush to tidy up before our guests arrive.

However, we can’t quickly clear up any messy elements of our finances before we meet with an adviser – and trying to do so could be risky and costly.

So, we must put our financial cards on the table and try not to worry about what the adviser will think of them. Very few people have well-organised finances – until they find a good adviser or coach and act on that advice.

If you had everything in order, why would you need advice?

Remember, even the rich and famous make enormous mistakes with their money – like these (just a few of the many) who, sadly, lost fortunes in Bernie Madoff’s Ponzi scheme.

• Steven Spielberg: Academy Award-winning director.

• Jeffrey Katzenberg: Co-founder of DreamWorks Pictures alongside Spielberg.

• Eric Roth: American screenwriter for “Forrest Gump” and “A Star Is Born”.

• Larry King: Emmy-winning American television and radio host.

• Kevin Bacon and Kyra Sedgwick: Golden Globe-winning actors and married couple

• Zsa Zsa Gabor: Former Miss Hungary (1936), starred in Moulin Rouge (1952).

• John Malkovich: American actor, director and producer.

(The information is all in the public domain)

Be aware also that a few years ago, hundreds of famous sportspeople, comedians, and other stars lost money in tax avoidance schemes in the UK.

The key point here is that you should not worry about the current state of your finances: they are what they are.

You just need to find someone competent in money matters to review your situation and give you a financial health check. And, like any health check, this is best done before it’s too late.

Reason 8: We don’t have control of the money in our family

If you have a partner, adult children or elderly parents (and you’re not yet doing so), you and they could benefit enormously from discussing some aspects of your financial plans.

In the future, we’ll offer more ideas for day-to-day money planning with your partner if you need them. So, please drop us a line if you’d like to see those.

For now, on your longer-term finances, be aware that you need to decide whether to:

- Undertake all your money planning together.

- Consider your unique personal situation and goals first, then come together to discuss your shared financial goals.

- Keep all the details of your financial situation and plans – to yourself.

There are no right or wrong answers here – although, if you’re in a committed long-term relationship, it makes sense to share your broad approach to money planning with your partner, even if you don’t share the details.

Also, be aware that intergenerational wealth planning can yield some remarkable tax savings. Wealthy parents or grandparents often wish to pass wealth to children or grandchildren.

And making gifts during one’s lifetime (currently) offers much more than just tax savings. If you’re making a gift, you’ll also enjoy seeing your loved ones benefit from it. Just be sure to talk to an adviser with specialist knowledge in this area so you can arrange those gifts without triggering unnecessary income or capital tax bills!

And be aware that this is not just about gifting money.

You’ll need to invest some of your time to properly explore what you (and any partner or broader family – if you want them involved) want for the future.

Reason 9: We don’t think this is a problem for today

We only accept change when we’re faced with necessity. And we only recognise necessity when a crisis is upon us.

This insight from Jean Monnet surely resonates for most of us in our personal lives.

Jean Monnet was a French Economist and diplomat who led much of the re-planning of Europe after World War II.

Of course, some shocks to our finances are unavoidable and unpredictable. And when a breadwinner (or child carer) in a family is struck down by illness, accident or death, the financial consequences for the rest of the family can be dire.

Thankfully, because these are rare events, it costs very little to insure our lives and health against the financial impact. Or, rather, the cost is low, as long as we arrange these insurances while we have reasonably good health.

And given we can’t know when such a disaster might strike, it makes sense to set up these vital (life and health) insurances as soon as possible.

What’s more, in the UK, you’ll probably save money on these insurances if you arrange them through a professional adviser.

Beyond the risks to our life and health, our common money crises arise more slowly. And, like the boiling frog*, we seldom notice the change creeping up on us until it’s too late.

- Charles Handy uses the boiling frog metaphor in his book The Age of Unreason to describe our inability to react to significant but slow-moving environmental changes. The idea is that a frog – placed in a pan of cold water, which is slowly heated – will not sense any danger and allow itself to be killed and cooked.

Apparently, the story is a myth, and a frog in such a situation would jump out. So, perhaps it’s only humans who have this problem!

It’s our status quo bias that gets us.

Making significant changes to our finances requires analysis and decision-making, which can be hard work.

The status quo feels like an easier option, and it is in the very short term. We avoid the pain of the effort and any regret we might feel when we reveal our financial challenges.

For years, research has shown that most people prefer not to think about their finances. But avoiding the subject clearly doesn’t help. And relatively recent reports show that up to 90% of people lose sleep over money worries.

Our gradually occurring money crises (like those affecting our health and well-being) arise from how we spend our time and money.

Yes, we can choose to eat, drink and be merry if we like.

While we have money in the bank (or credit on the card), we are free to shop, gamble, smoke, watch TV and play games – and those activities might make us merry for a while. However, we all know our happiness won’t last if we do these things to excess.

A tipping point always arrives when we start losing the things we value most in life: Our health, our relationships and the savings we need for our life goals, like buying a house or building future funds for ourselves or our loved ones.

Suddenly, we realise that what we thought made us happy has little or no value at all.

It’s true that saving to build wealth over the long term is a challenge – precisely because it’s such a long-term game. The emotional part of our brains (our ‘Chimp’*) is impatient and grabs the offers of short-term pleasure.

- The Chimp is a key part of the brain model offered by Professor Steve Peters, Psychiatrist, acclaimed mind coach to Olympic champions, and author of Chimp Paradox.

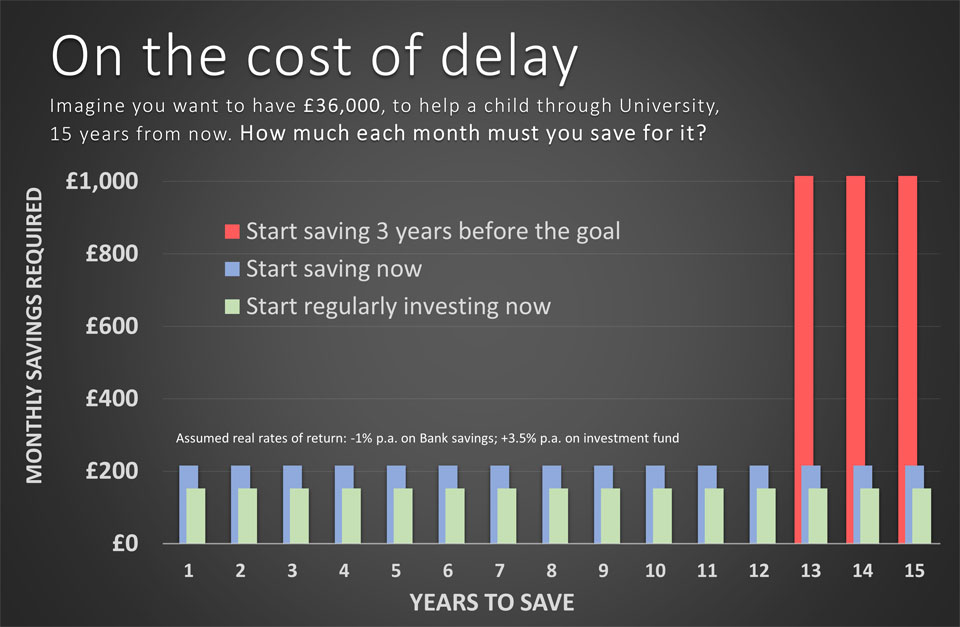

It does require patience to save and invest in our pension fund for 30 years or to build a big fund of money over, say, 15 years, to help a child through University… or to take six months off work – to travel the world!

But what choice do we have?

Leaving our longer-term savings to the last minute only guarantees one thing – that our big financial life goals become impossible to achieve – as shown here.

Reason 10: We think financial planning is simple, common sense

So, here’s the last reason we’ll offer, for now, about why we don’t talk about money – or take financial advice.

We assume we don’t need to!

It’s quite common to believe that financial planning is just common sense.

That’s wrong, but it’s what you’ll hear from thousands of unqualified, self-proclaimed money gurus and influencers. You know them – they claim to have simple answers to all your money worries.You only have to like, follow, and subscribe to their Social Media channel to get regular access to their ‘one-liner’ top tips.

What could be easier than that?

The problem is that one-liner tips are NOT personal advice.

Of course, this doesn’t matter to all of those #finfluenzas, some of whom are only there to earn income from advertising on their YouTube or TikTok channels. And yes, YOU (or your attention) is the product they’re selling to the advertisers.

We all know that now.

The truth is that managing all aspects of your money is seldom simple, and researchers in financial literacy are clear about that.

It’s hard to manage our money – because we need to:

• Keep our income above our expenditure.

• Juggle the repayments on a mortgage with those to pay down other debts charging higher interest.

• Cope with general increases in interest rates.

• Build funds in accessible savings accounts to cover emergencies.

• Save and invest for our medium and longer-term life goals.

It’s not simple at all.

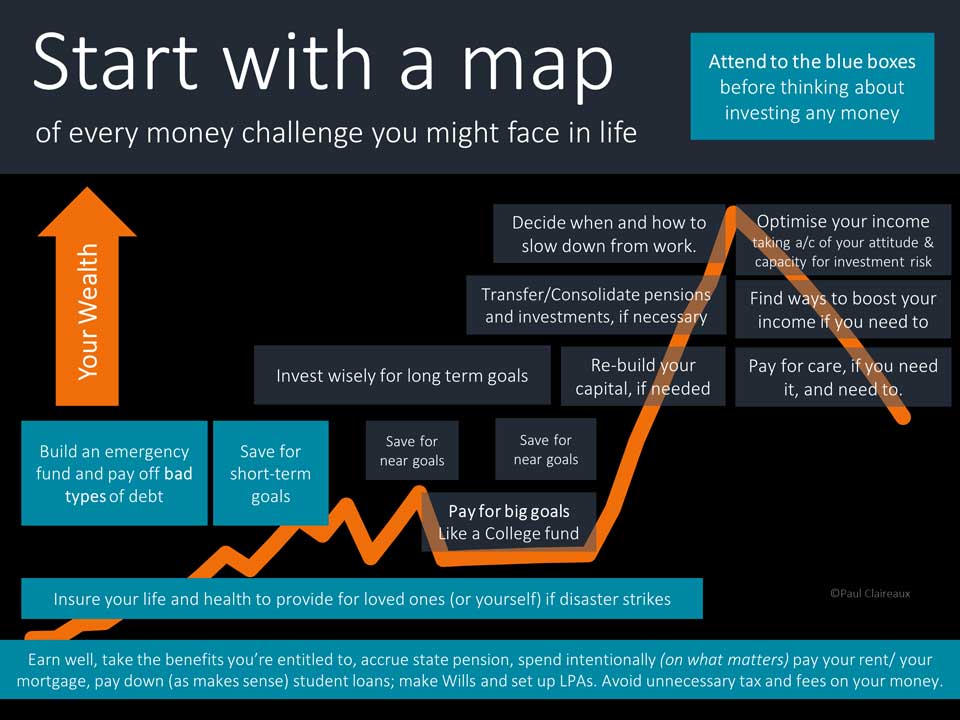

Look at this map of the money challenges most people face throughout life.

Thankfully, we don’t have to deal with all those challenges at once.

But Financial Planning is not common sense.

There’s no common-sense way to work out your key savings numbers. You need to know how to run the calculations using sensible assumptions.

There’s no common-sense way to design a sound strategy for achieving your financial life goals. You need to know how to make good choices about the savings and investment boxes you hold and the funds you put inside those boxes.

So, there are a great many traps for the unwary if you:

• Fail to set up those insurances.

• Fail to make a will or set up your powers of attorney.

• Pay too much on your mortgage or other loans.

• Allow your wealth to be dragged down by inflation – or poor-performing (or excessively expensive) funds.

As Nobel Prize-winning economist Daniel Kahneman often pointed out:

Common sense answers to complex questions (about money, work, life and love!) are often wrong.

Bottom lines and next steps

We believe that the common-sense trap is essential to understand. So, we’ve written a whole ‘About Money’ article on this for you to read here.

For now, let’s stop and think about this:

How could there possibly be one common-sense solution to your unique set of personal financial challenges?

How could one solution (summarised in a 20-second video on TikTok) take account of your unique financial circumstances, attitude to money (and risk) and your ambitions in life?

That’s just nonsense!

The only financial plan you need is one tailored to your personal needs.

No video, book, podcast or article can give you that – because the author of those works knows nothing about you!

On the other hand, as Financial Planners, we will get to know you – and listen to what you want for your future. We’ll explain your financial challenges and the solution ideas, and hopefully, in plain English.

We won’t pretend anything is simple – if it’s not.

Instead, we’ll work with you to design and implement your personal financial plan.

And that is what you need to achieve more of your unique (financial) life goals.

So, if that sounds interesting, talk to Create Wealth Management.

And thanks for dropping in